A Lifetime of Financial Milestones: Navigating Key Life Events 2025

A Lifetime of Financial Milestones: Navigating Key Life Events

To view complete list of milestones and download pdf, click below

Life is a journey filled with significant milestones, each bringing unique financial considerations. From the moment we are born to our golden years, various events trigger important financial decisions that can significantly impact our future well-being. Understanding these milestones and their associated financial implications empowers individuals to make informed choices and navigate their financial journey with greater confidence. This comprehensive guide outlines key financial milestones throughout a person’s lifespan, providing insights into the financial opportunities and considerations associated with each stage.

This guide will explore a range of milestones, from the early years of childhood, including the impact of education savings and the transition to adulthood, to the complexities of retirement planning, including Social Security benefits, Medicare enrollment, and estate planning. We will delve into key moments such as the age of majority, eligibility for government benefits, and the importance of retirement savings strategies. By understanding these milestones and their financial implications, individuals can proactively plan for their future and make informed decisions about their finances.

Early Years: Building a Foundation

Birth:

- Milestones: Named as beneficiary of a 529 plan account and owner of UTMA/UGMA accounts.

- Financial Implications: This marks the beginning of your child's financial journey. 529 plans offer tax advantages for funding future education expenses, while UTMA/UGMA accounts provide a means to save and invest for your child's future needs. It's crucial to understand the tax implications and restrictions associated with these accounts.

Age 13:

- Milestone: Child no longer eligible for the Child and Dependent Care Credit.

- Financial Implications: As your child grows, you may need to adjust your budget and financial planning accordingly to accommodate increasing expenses related to extracurricular activities, sports, and social events.

Age 17:

- Milestones: Child no longer eligible for the Child Tax Credit.

Age 18:

- Milestones: Age of majority in most states. Age of termination for some UGMA and UTMA accounts. Child no longer subject to Kiddie Tax (unless a full-time student).

- Financial Implications: Reaching the age of majority brings significant responsibilities. Your child may now be legally responsible for their actions and may need to start managing their own finances. This period often involves significant life changes, such as starting college or entering the workforce. Financial considerations include managing student loans, building credit, and establishing a budget for independent living. It's crucial to discuss financial literacy and decision-making with your child during this transition.

Age 21:

- Milestones: Age of majority in some states. Age of termination for some UGMA and UTMA accounts.

- Financial Implications: This age often marks a transition to greater financial independence. Young adults may be focusing on career development, building an emergency fund, and planning for long-term financial goals.

Age 24:

- Milestone: Child who is a full-time student no longer subject to Kiddie Tax.

- Financial Implications: This can have tax implications for the student and their family.

Age 26:

- Milestone: Adult child may lose parents' health insurance coverage under the Affordable Care Act.

- Financial Implications: This milestone highlights the importance of securing health insurance coverage. You may need to explore options for obtaining health insurance through an employer, the marketplace, or other avenues.

Middle Age: Building Wealth and Planning for the Future

Age 50:

- Milestones: Eligible to make catch-up contributions to retirement accounts [e.g., IRA, 401(k), 403(b), 457]. Eligible for Social Security benefits as disabled widows/widowers.

- Financial Implications: Reaching age 50 opens new opportunities to boost your retirement savings. Catch-up contributions allow you to contribute a larger amount to your retirement accounts, which can significantly increase your retirement income. Additionally, eligibility for Social Security disability benefits as a widow/widower can provide crucial financial support during a challenging time.

Age 55:

- Milestones: Eligible to make catch-up contributions to a Health Savings Account (HSA). Eligible for penalty exceptions for certain withdrawals from retirement accounts.

- Financial Implications: Catch-up contributions to an HSA can help you save more for qualified medical expenses, offering greater financial security for healthcare costs in the future. The penalty exceptions for certain withdrawals from retirement accounts provide flexibility in accessing your retirement savings in case of unforeseen circumstances, such as a major medical expense or a job loss.

Age 59 1/2:

- Milestones: Eligible to withdraw from IRAs without the 10% early distribution penalty.

- Financial Implications: Reaching age 59 1/2 provides access to tax-advantaged retirement accounts without the 10% early withdrawal penalty. This can be a valuable option for accessing funds in case of an emergency or to supplement income during retirement.

Age 60:

- Milestones: Eligible to make increased catch-up contributions (ages 60-63) to certain retirement accounts [e.g., 401(k), 403(b), SIMPLE, etc.]. Eligible to claim Social Security survivor benefits as a widow/widower (early, at a reduced rate).

- Financial Implications: These additional catch-up contributions can provide a significant boost to your retirement savings in the years leading up to retirement. Eligibility for Social Security survivor benefits can provide crucial financial support for widows/widowers.

Retirement Years: Pursuing Financial Independence

Age 62:

- Milestones: Eligible to claim Social Security retirement benefits (early, at a reduced rate). Eligible to qualify for a reverse mortgage.

- Financial Implications: This is the age when you may start considering claiming Social Security benefits. However, claiming early will result in a reduced monthly benefit.

Age 63:

- Milestone: Final year to make increased catch-up contributions (ages 60-63) to certain retirement accounts [e.g., 401(k), 403(b), SIMPLE, etc.].

- Financial Implications: This is the last opportunity to maximize your retirement savings with increased catch-up contributions.

Age 64+9 Months:

- Milestones: Start of the Initial Enrollment Period for Medicare.

- Financial Implications: This is the period to enroll in Medicare if you are eligible. Understanding Medicare coverage options and making informed decisions about your healthcare plan is crucial during this time.

Age 65:

- Milestones: Eligible for non-medical withdrawals from a Health Savings Account (HSA) without penalty. Eligible for coverage under Medicare (assuming timely application).

- Financial Implications: This is the age when you can withdraw funds from your Health Savings Account (HSA) for non-medical expenses without penalty. You also become eligible for Medicare coverage, which can provide significant financial relief for healthcare costs.

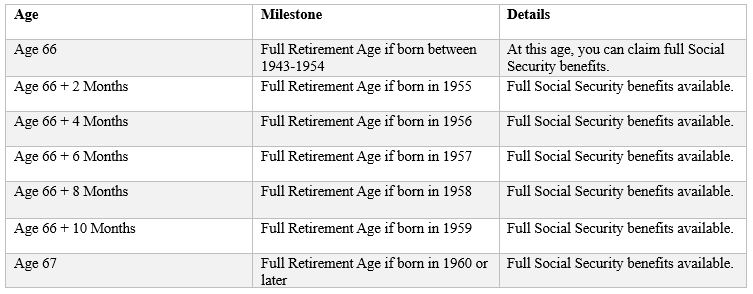

Age 66 - 67:

- Milestones & Financial Implications: See chart above.

Age 70:

- Milestones: Maximum Social Security benefit is reached. Eligible to make a Qualified Charitable Distribution.

- Financial Implications: Claiming Social Security benefits at age 70 maximizes your monthly benefit amount. Qualified Charitable Distributions (QCDs) allow you to transfer funds directly from your IRA to a qualified charity, which can provide tax benefits.

- Milestones: Eligible to make a Qualified Charitable Distribution.

- Financial Implications: Qualified Charitable Distributions (QCDs) allow you to transfer funds directly from your IRA to a qualified charity, which can provide tax benefits.

Age 70 1/2:

Age 73:

- Milestone: Required Minimum Distribution Age, if born before 1960.

- Financial Implications: You are required to begin taking Required Minimum Distributions (RMDs) from your retirement accounts if you were born before 1960.

Age 75:

- Milestone: Required Minimum Distribution Age, if born in 1960 or later.

Navigating the complexities of financial planning throughout your life requires careful consideration of key milestones and their associated implications. From the early years of childhood to the challenges of retirement, understanding these milestones empowers individuals to make informed decisions and help them achieve their long-term financial goals. By proactively planning for these events, individuals can optimize their financial well-being and navigate life's transitions with greater confidence.

At Total Clarity Wealth Management, we are dedicated to guiding our clients through every stage of their financial journey. Our team of experienced financial professionals provides comprehensive planning and investment management services tailored to your unique needs and goals. We believe in building long-term relationships with our clients based on trust, transparency, and a shared commitment to success.

Contact us today to schedule a consultation and explore how our expertise can help you pursue your financial aspirations.

Securities offered through LPL Financial, Member FINRA / SIPC. Investment advice offered through Total Clarity Wealth Management, Inc., a registered investment advisor and separate entity from LPL Financial.

This information is not intended to be a substitute for specific individualized tax or legal advice. We suggest that you discuss your specific situation with a qualified tax or legal advisor.

Prior to investing in a 529 Plan investors should consider whether the investor's or designated beneficiary's home state offers any state tax or other state benefits such as financial aid, scholarship funds, and protection from creditors that are only available for investments in such state's qualified tuition program. Withdrawals used for qualified expenses are federally tax free. Tax treatment at the state level may vary. Please consult with your tax advisor before investing.

Contributions to a traditional IRA may be tax deductible in the contribution year, with current income tax due at withdrawal. Withdrawals prior to age 59 ½ may result in a 10% IRS penalty tax in addition to current income tax.